The World's Largest Planned Data Center Is Running Into Trouble

Last summer, Fermi America raised $746 million to build the world's largest data center. Satellite images show the project is at least a year behind the schedule projected in its IPO filing.

Update, April 19, 2026: On April 17, after this story was finalized, Fermi announced that co-founder and CEO Toby Neugebauer was departing the company effective immediately.

Last October, Fermi America raised $746 million in an IPO to build what it claimed would be the largest data center in the world. The company successfully pitched investors on a massive campus it tentatively called the President Donald J. Trump Advanced Energy and Intelligence Campus. (The company now generally refers to it as Project Matador.)

Speed and scale were key to Fermi’s pitch. The company told investors it expected to make $1.5 billion in revenue for every 1 GW of capacity built. It said it expected to launch the first one million square feet of space by April 2026 and generate 1 GW of power by the end of 2026. Fermi originally pitched an 11 GW campus; it later increased the targeted capacity to 17 GW.

On its website, the company says that the “initial phase of construction [is] already complete.” But the company has still yet to begin constructing its first buildings, according to Cleanview’s satellite tracker.

Across the country, data center developers are racing to hire construction workers. At the site of OpenAI’s Stargate campus in Abilene 5,000 workers are working through the night to finish the 1.2 GW campus. At Fermi’s site in Amarillo, the workforce has been shrinking, according to local media reports.

In February, The Amarillo Tribune reported rumors of layoffs among construction workers at the site. In response, Fermi’s CEO Toby Neugebauer said that the company was awaiting a ruling on its final Clean Air Permit. “We completed our first phase so fast that we paused construction temporarily,” he said in a statement. A company spokesperson later told KAMR that Fermi still had 100 construction workers on site despite the pause.

Weeks later, on February 25th, Fermi announced that it had secured its air permit and posted a photo to its website with a caption that read, “First phase of construction almost complete.”

Satellite images suggest the company hasn’t begun significant construction activity since then, however.

This is what Fermi’s data center site looked like in August 2025, the month before the company filed its IPO documents.

Two months later, the company went public. That same month, construction workers began clearing land at the site.

By February—the month that Fermi said it had paused construction—this is what the site looked like.

Two months after construction was supposed to resume—and the month that Fermi originally said it would finish its first one million square feet of space—the site looks essentially the same.

Fermi America isn’t the only company attempting to build a mega-campus like this. More than 70 gigawatt-scale data centers have been proposed in the US since the launch of ChatGPT, according to Cleanview’s data center tracker. (1 GW is equivalent to the power demand of an entire city).

Many of these data centers are already under construction, which gives us the ability to compare Fermi’s first 6 months of progress to that of other companies.

Meta announced its 5GW Hyperion campus in Richland Parish, Louisiana in December 2024 and began clearing land at the site two months later. Here’s what the site looked like 6 months later.

In June 2024, OpenAI’s partner Crusoe began building its 1.2 GW Stargate campus in Abilene, Texas. Within six months, Crusoe finished its first building shell and was putting the roof on the second building. The company launched its first 980,000 square foot phase (200 MW) in September 2025, 15 months after it began construction.

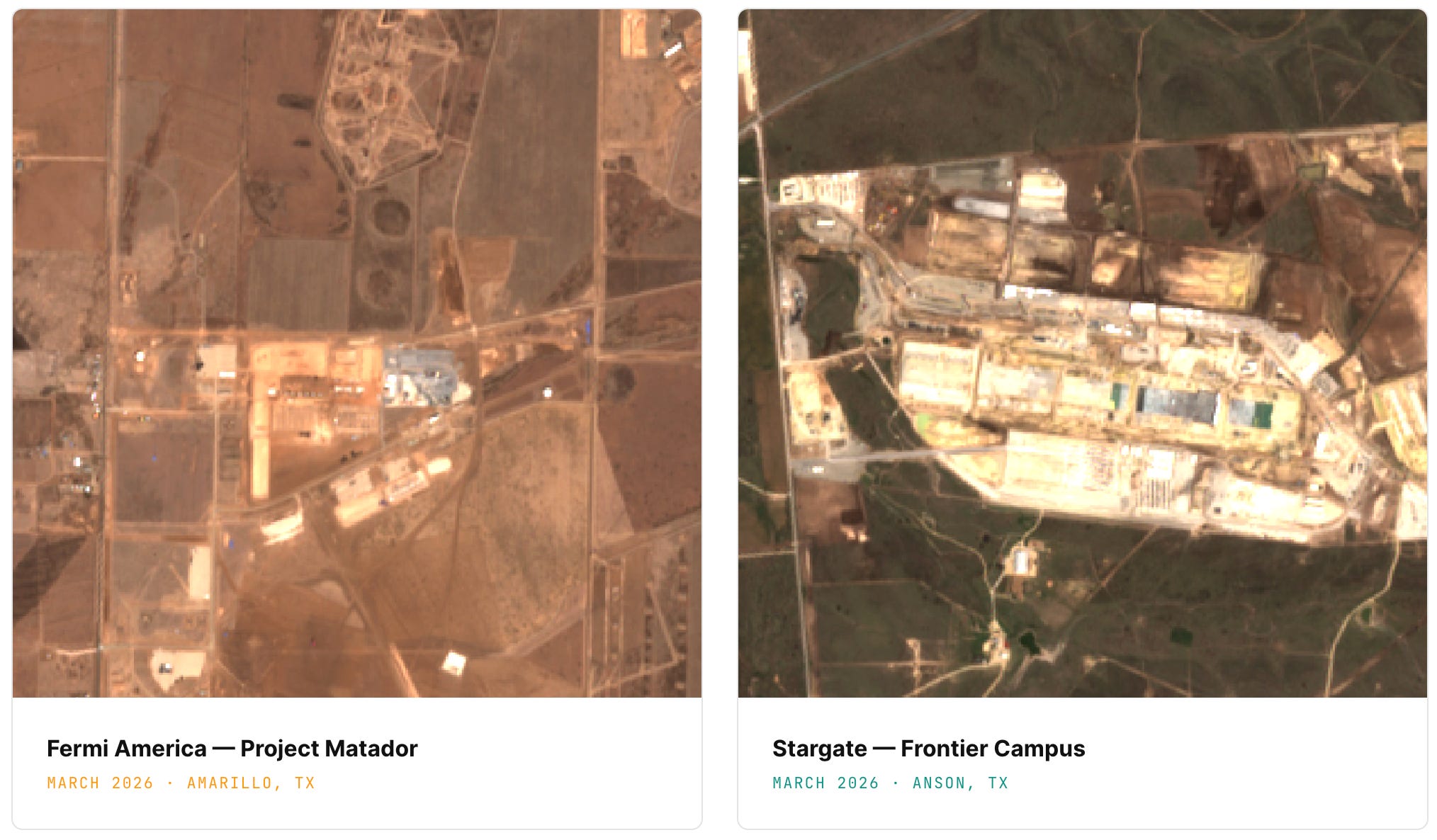

50 miles north of Abilene, Vantage Data Centers is building the second Stargate campus for OpenAI. The 1.2 GW project began construction in September 2025. Here’s what the site looked like 6 months later.

The Rise and Stall of the Largest Data Center in the World

Six months ago, Fermi America raised one of the largest data center IPOs in history.

The company was co-founded by Toby Neugebauer, the son of retired Republican Congressman Randy Neugebauer, whose former district includes the Amarillo area where Project Matador sits. Rick Perry, the former governor of Texas and Trump’s first Secretary of Energy, is also a co-founder. When Fermi went public in October 2025, Perry’s 2.5% stake was worth roughly $540 million. Neugebauer’s 28% stake was worth approximately $6 billion.

From the start, Fermi has touted its proximity to the White House.

“If the President of the United States wants to move fast [and] wants to have a shovel-ready project in the very near term, Project Matador is his first, second, and third great choice.”

— Toby Neugebauer, Fermi America CEO

The company tentatively named the campus after the president. On its first earnings call, Neugebauer disclosed that Energy Secretary Chris Wright and Interior Secretary Doug Burgum had personally intervened to help the company secure Siemens turbines during trade negotiations with Germany. Neugebauer said Siemens “wanted confirmation that this would make the United States happy” and that Fermi received “a massive push-push by the United States of America” to get the deal done.

In July 2025, Trump signed an executive order designating AI data centers at DOE facilities as critical defense infrastructure — directly benefiting Fermi’s site adjacent to the Pantex nuclear weapons plant. Neugebauer told investors that “if the President of the United States wants to move fast, wants to have a shovel-ready project in the very near term, that Project Matador is his first, second, and third great choice.”

In November, the company announced it had signed a $150 million funding agreement with an unnamed, investment-grade tenant. Neugebauer told Business Insider that the tenant was Amazon. (After the story published, Fermi issued a statement saying they “categorically deny Business Insider’s claim.”)

Things began to unravel quickly. In Fermi’s first investor presentation in November, the final slide showed that tenant negotiations were behind schedule. When an analyst pressed for details, Neugebauer said they were just three weeks behind and would make up the time. Three weeks later, the exclusivity window on the deal expired. Two days after that, the tenant formally pulled out. The company’s stock immediately plummeted 34%.

In January, a class action lawsuit was filed alleging that Fermi had overstated tenant demand and failed to disclose how dependent the project was on a single tenant’s funding commitment.

In its second earnings call with investors, on March 30th, company executives said they still hadn’t secured a tenant. The CFO said they wouldn’t invest significant capital into construction until they had. He told investors Fermi “could be forced to… surrender collateral to preserve liquidity.” In other words, the company may need to sell some of the Siemens turbines that two cabinet secretaries helped secure.

When a Cantor Fitzgerald analyst asked for more details, Neugebauer jumped in to walk it back. He said giving up turbines was “not our intention whatsoever,” and added that he’d “auction off my two boys first before I would let one of these gensets go.”

On April 17, two and a half weeks after that earnings call, Fermi announced Neugebauer’s immediate departure. Shares fell as much as 31% in post-market trading.

A Year Behind and Counting

Fermi still has a long way to go before it can generate revenue. In order to begin construction and secure project financing, the company needs to find a tenant. Even after that, building a data center at this scale takes time. Crusoe’s first Stargate campus in Abilene took 13 months from the time it began “vertical construction” to going live, with construction running 24 hours a day. That was for an initial 200 MW phase, which is a fraction of the 1,000 MW Fermi is targeting.

If Fermi secured a tenant this month and replicated Crusoe’s speed, it would bring the first buildings online in May 2027—a full year after the initial timeline projected in its IPO filing.

How we did this analysis

This report is based on Cleanview’s monthly satellite tracker, SEC filings (8-K, 10-K), earnings call transcripts, investor presentations, and news reporting from the Amarillo Tribune and Business Insider.

Cleanview tracks more than 850 planned data centers in the US. For each site, we have satellite imagery dating back to 2022 giving us the ability to track progress over time. We used these satellite images to analyze Fermi’s progress compared to other data center developers.

You can try our new satellite tracking feature for free here:

While satellite imagery provides a clear snapshot of physical ground-breaking, this report fundamentally overlooks the most critical value drivers for a project of this scale: Regulatory Moats and Supply Chain Integrity.

In the nuclear and utility-scale AI sectors, a project’s worth is measured in permits and partnerships long before the first reactor vessel arrives. By focusing solely on "dirt piles," this analysis ignores three massive pillars:

The Licensing Moat: The NRC’s fast-track EIS (Environmental Impact Statement) and COL progress are monumental regulatory milestones. Securing a site that is federally recognized for nuclear deployment is a generational asset that doesn't show up on a satellite feed but is the primary requirement for DOE loans and institutional financing.

Energy Optionality (TCEQ Permits): Ignoring the 11GW of TCEQ Air Quality Permits (6GW secured + 5GW in progress) for natural gas backup is a major oversight. This gives the project immediate viability and power-gen rights in the ERCOT grid, providing a bridge to nuclear operations that stabilizes the project's financial outlook.

Global Strategic Alliances: You cannot build a project of this magnitude without a world-class supply chain. The strategic commitment from Doosan Enerbility (one of the few global forges capable of producing AP1000 components) and Hyundai E&C (a leader in nuclear EPC) provides a level of technical backing that far outweighs the current state of on-site construction.

A project like Matador is won or lost in the regulatory and procurement phase. To judge a 60-billion-dollar nuclear-AI infrastructure play solely by its current brick-and-mortar footprint is to fundamentally misunderstand how modern energy-megaprojects are developed.

The real story isn't just what's happening on the ground—it's what's happening in the "invisible" layers of federal licensing and global supply chain alignment.